The Relationship Between Claims and Home Insurance Rates

Let’s say you experience a hailstorm in Wichita, KS. You call a roofing expert to perform an inspection of your roof, and they suggest that your 10-year-old roof experienced hail damage that warrants filing an insurance claim. You successfully file, your roof gets replaced, but you notice that it had a negligible effect on your premiums. Why?

- Filed claims resulting from an “Act of God,” like hail, won’t typically increase your premium as significantly as a kitchen fire, for example. If you live in Wichita, KS, hail damage won’t surprise your carrier like a sudden kitchen fire would. The risk of hail is accounted for in your premiums.

- However, a pattern of frequent claims, even for weather events, is very likely to raise your premiums. If you file four claims in one year, your carrier assumes you’re more likely to file more, making you a higher liability customer.

So what can be done to lower your premiums? And how does your carrier determine your rates to begin with?

Before addressing these questions, they need to be prefaced by two important disclaimers.

First, “Ask your doctor about [x]” works for medication commercials because your doctor understands your personal health better than any marketing team. The same principle applies to your homeowner’s insurance. You and your insurance agent or carrier understand your home and your situation better than anyone else. This article highlights common factors that influence insurance premiums and trends worth knowing. For advice, contact your insurance provider directly.

Second, Insurance companies determine your premiums based on risk. From your carrier’s perspective, paying premiums without filing claims makes you a lower-risk customer. Filing a claim shifts that balance. That doesn’t make insurance companies the enemy – they’re a business that balances risk and profit. The more your goal of protecting your home aligns with your carrier’s goal of minimizing claims, the better chance you have of lowering your premiums.

This article will clarify the many variables that influence home insurance premiums and highlight common methods of reducing premiums.

Navigating Home Insurance Premiums

What Factors Influence Home Insurance Premiums

Why Your Roof Plays a Key Role in Your Insurance Costs

Roof Improvements that may Lower Insurance Premiums

What to Know After Filing a Roof-Related Insurance Claim

Law & Ordinance Coverage

Key Takeaways

What Factors Influence Home Insurance Premiums?

Every carrier evaluates your home differently. Your location can affect your fundamental risk (e.g., natural disasters) and your particular risk (e.g., theft and house fires). Some fundamental risks, such as inflation, are going to affect your premiums irrespective of your location. Even at your location, carriers might weigh these risk factors differently. Most carriers use proprietary calculators to determine rates, so each carrier can provide radically different rates for the same dwelling.

For homeowners whose sole concern is the absolute lowest premiums, below is a reliable way to obtain them:

-

- Move to Alaska, Hawaii or Delaware.

- Build a 5’ x 5’ shack with no plumbing, no HVAC, and no electrical wiring.

- Use fireproof, waterproof, and reality-proof materials.

- Cross your penny-pinching fingers and hope your home never sees rain, drought, or sunshine.

This obviously isn’t realistic. Nobody should blindly chase the cheapest premium at the expense of quality coverage that protects them.

Instead, ask yourself and your carrier, “How can I lower my premiums without sacrificing the protection I need?”

Your Home’s Age, Condition, and Materials

Older homes and homes in poor condition will generally receive higher rates. That’s because age and wear introduce more potential for problems, and more problems mean more risk for your carrier.

If you’ve filled out an online quote form or applied for homeowner insurance, you likely learned about your roof’s age, your home’s wiring, and your plumbing materials in the process. Insurers are exhaustive because this information helps them predict how likely you are to file a claim.

Beyond your home’s age and materials, your carrier may also consider exterior features or potential risks on your property.

Attractive nuisances like pools or wood-burning fireplaces will consistently increase homeowner insurance premiums. Dormers or cornices might affect premiums. Some carriers spring your premiums up if you own a trampoline, while others let you bounce by without penalty.

Your Claims History

Before filing a homeowner’s insurance claim, it’s always worth speaking with a professional. Every claim you file gets logged in a national database called CLUE (Comprehensive Loss Underwriting Exchange).

CLUE is accessible by all major insurance carriers, meaning your claims stick with you, even if you switch insurers. A single weather-related claim may not influence your premiums, but a pattern of claims over several years suggests to carriers that you’re a high-risk policyholder – even if each claim was weather-related.

Reports are available upon request that detail your past claims and the credit reporting that underwriters review to determine your rates. This allows you to confirm the accuracy of their information and dispute errors that might cost you.

Understanding the Date of Loss

Claims typically need to be filed within a year of a damaging weather event, such as hail or whole gale winds. This is the date of lossCompliance - The date of loss is the date a specific storm or weather event caused damage cited in an insurance claim. More, and it will be referenced by your carrier when your claim is reviewed. A weather event that occurs outside of your policy’s coverage period is likely to be denied. Carriers often use their own weather reports to verify, or dispute, the date of loss. Experienced roofing professionals use similar tools to pinpoint your roof’s most significant hail event with the coverage period. This ensures that your claim aligns with verifiable weather data.

Local Weather Risks and Geographic Location

What potential premium-reducing changes have in common is that they lower the likelihood of you submitting a claim. This is the common denominator for everything that influences premiums, from the age of your home to your claim history – even your credit score. If it affects how likely you are to submit a claim, it will affect your premiums.

Close-up of an asphalt shingle roof with a white chalk circle marking a hail impact, showing granule lossRoof Problems - Degranulation (granule loss) is the loss of protective granules from the surface of asphalt roof materials such as shingles and modified bitumen. More and slight indentation.

In the lower Midwest, hail dramatically affects premiums. A plurality of home insurance claims nationwide are incited by hail damage. Kansas consistently has one of the five highest average annual premium costs as a result. The potential for hail significantly increases the likelihood of filing an insurance claim, and the potential for tornadoes significantly increases the cost of the average claim. These factors inflate premiums in Kansas, Oklahoma, and Nebraska.

For homeowners in the lower Midwest, this risk makes choosing the right roof and managing your claims history even more important.

Why Your Roof Plays a Key Role in Your Insurance Costs

Insurance premiums are influenced by myriad factors, but most of them boil down to two key questions:

-

- How likely are you to file a claim?

- How expensive would that claim be?

In the lower Midwest, hail plays an outsized role in both: it raises the chances you’ll need to file a claim, and hail damage is typically costly. A home that can weather the storm – literally – is less likely to trigger a claim, and any claim that does happen may be less severe.

Roof Improvements that may Lower Insurance Premiums

Impact-Resistant Shingles

UL Solutions Inc. independently tests building materials for various safety functions, but we’ll focus on what can decrease your premiums: impact resistance.

Most asphalt shingles have a Class A fire rating, so this potential discount is likely presumed by your carrier if you have an asphalt shingle roof. To get an idea of what insurance premiums look like without a fire-resistant shingle, read this article examining wood shake roofs.

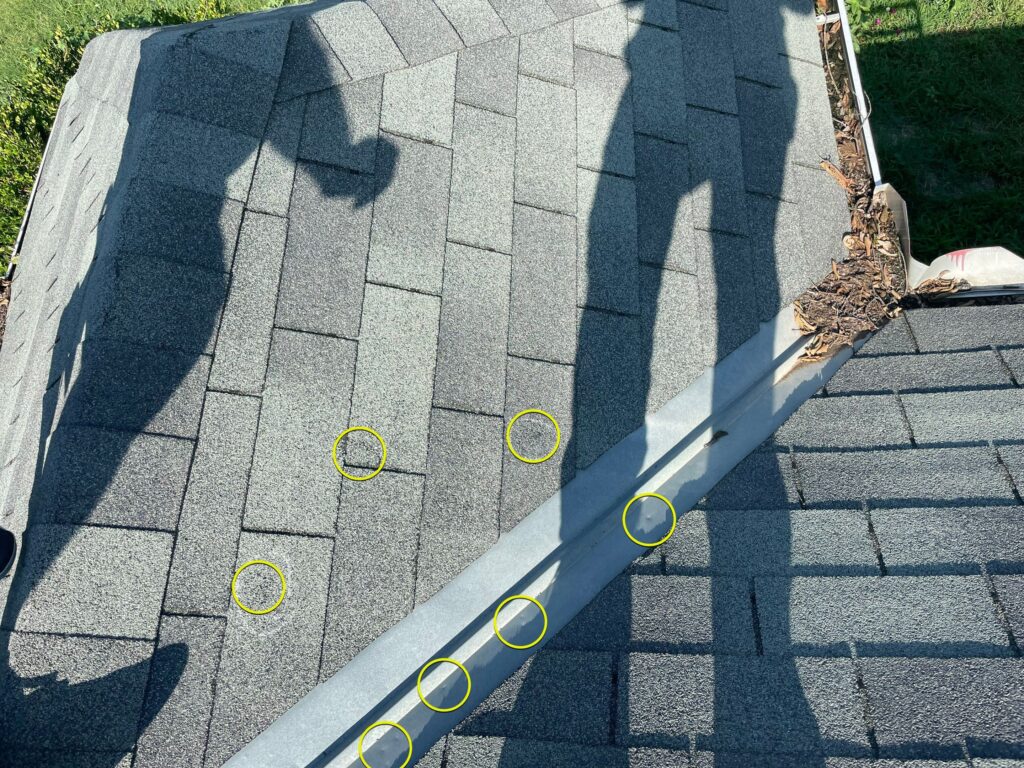

Yellow circles highlight hail impacts on an asphalt shingle roof.

UL Solutions collaborated with insurance companies and shingle manufacturers to develop UL 2218, a test that drops a steel ball bearing onto a shingle from a specific height. This effectively simulates hail impact and allows UL Solutions to assess the impact resistance of shingles.

There are many ways our roofing experts assess a roof to determine the viability of an insurance claim. One of the most common signs of damage is granule loss produced by hail impacts. Impact resistant shingles are less likely to incur damage from hail impact, meaning your roof is less likely to incur a claim.

Class 3 Shingles

Class 3 impact-resistant shingles are the lowest-scoring class of shingle that can enable premium savings. The Midwest experiences hail, so most carriers in the Midwest will reduce premiums for homeowners that invest in impact-resistant shingles. Our preferred manufacturer, GAF, earned a Class 3 impact resistance grade on its Timberline HDZ asphalt shingles. This rating is retroactively applied to all HDZ shingles installed in 2024 and beyond.

To illustrate how UL Solutions’ test accurately captures a shingle’s impact resistance, let’s break down the numbers.

We’re going to calculate the impact force of a steel ball bearing striking an asphalt shingle to understand just how much abuse a shingle can endure in a severe hailstorm.

First, we need the potential energy of the ball. The ball bearing weighs 0.85 pounds, and we’ll drop it from 17 feet. Potential energy is simple: multiply weight by height. That gives us: 0.85 lbs x 17 feet = 14.4 foot-pounds of potential energy.

Next, we calculate the impact force. This will depend on how much the shingle and underlayment “give” when the ball hits. In this case, we’ll use a stopping distance of 0.05 inches – reasonable for an asphalt shingle over solid wood decking. Converted to feet, that’s: 0.05 inches / 12 = 0.00417 feet.

To find the impact force, we divide the potential energy by the stopping distance.

14.4 foot-pounds / 0.00417 feet = approximately 3,450 pounds of force.

That’s the equivalent of a mid-sized sedan concentrated onto a single point. Our estimates are on the upper-end, assuming minimal give and no rebound. But the UL2218 test is intense, and many insurance carriers will discount premiums for homeowners with impact resistant shingles as a result.

Class 4 Shingles

Class 4 impact-resistant shingles survived a bigger ball dropped from a greater height. If your insurance carrier offers discounts for impact-resistant shingles, Class 4 shingles typically qualify for the biggest discounts.

That discount can be substantial. Some of our customers have benefitted from premium reductions of up to 38%, saving them $1,800 annually. For one customer, Class 4 shingles reduced premiums by $1,200 while Class 3 saved them $1,100, making Class 3 the better value for them.

On the other hand, some customers see little or no change in their premiums with impact-resistant shingles. It all depends on your carrier’s policies, your location, and your home’s overall risk profile.

The best way to determine your potential savings is to call your insurance agent directly and ask:

- How much will class 3 impact-resistant shingles affect my premiums?

- How much will class 4 impact-resistant shingles affect my premiums?

- Do you offer a new-roof discount?

- Is there anything else that can lower my premiums?

Of course, there are more reasons than your potentially reduced insurance premiums to invest in impact-resistant shingles. If you intend to move, your home’s resale value can increase and the next owner of your home could benefit from a similar premium reduction. If you don’t plan on moving, impact resistant shingles are even more attractive. We have an article detailing when it’s worth upgrading to class 4 shingles. Reduced premiums are one of many reasons to consider a class 4 upgrade.

New Roof Discount

Some insurance companies offer a new roof discount, rewarding homeowners who upgrade their old roof. An asphalt shingle roof that’s weathered 20 years of storms and sun is a claim waiting to happen.

Going all day without eating doesn’t mean that you’ve conquered hunger: it means dinner’s going to be enormous. An old roof works the same way: it’s not defying damage, it’s just due for its next meal, and your insurance carrier knows it.

That’s why it’s smart to notify your carrier when you replace your roof. If they offer a new roof discount, they’ll need an invoice or completion certificate as confirmation before applying the discount to your policy. A new roof discount can reduce your premiums by 5% to 35% so it’s always worth checking with your agent. However, not all insurance companies offer a new roof discount, so it won’t independently justify a new roof.

What to Know After Filing a Roof-Related Insurance Claim

For any questions or concerns relating to your insurance, talk to your insurance agent. This section contains information that our customers often wish they knew.

If your rate is affected by filing a claim, this will be reflected at your next policy renewal date. How much your rate increases depends on:

-

- Your claims history.

- The severity of the damage.

- The type of claim.

- Other factors relevant to your carrier’s risk calculator.

Because insurance carriers generally use proprietary calculators to determine rates, it’s unlikely your agent can give you an exhaustive breakdown of risks and savings. But it’s reasonable to expect increased rates after filing a claim.

-

- It’s illegal for a contractor to waive or pay your deductible. If they break the law to earn your business, they’ll break your trust to keep it.

- An indirect way to mitigate increases to your insurance premiums is to make your insurance claims count. Experienced and reputable contractors can give you information that helps you determine whether a claim is worth filing or not. If you have high-deductible coverage or plan on moving, filing a claim might not be in your best interest.

- Inflation in material costs affects your premiums, even without filing a claim. Since 2020, inflation of building material cost has outpaced inflation. As of March 2025, material inflation rates continue to outpace inflation. Because of this, you might notice that your insurance premiums increase in 2025 despite your risk-factors remaining constant.

- The 2007 Greensburg, KS tornado cost insurance companies at least $153 million and barely influenced national insurance premiums. But the $55 billion incurred by last year’s hurricanes had a major effect on premiums nationwide. Where you live matters, but the more catastrophic the disaster, the more likely it is to influence every homeowner’s rates.

- Hurricanes Helene and Milton are big reasons why insurance companies are generally migrating toward ACV and away from RCV. They want to reduce claims costs. Learn more about the difference between ACV and RCV policies.

Considering Law & Ordinance Coverage

Law and ordinance coverage can increase your premiums, but it can greatly reduce your out-of-pocket if a covered peril exposes code deficiencies in your older home.

For example:

If your home has spaced roof decking and local building codes require solid decking, law and ordinance coverage will typically cover the cost of upgrading to OSB or plywood during a covered roof replacement.

Close-up view of a homeowner’s roof with the old shingles removed, exposing aged spaced decking with wide gaps between wooden planks. Law and Ordinance coverage would likely cover the addition of up-to-code decking in this case.

This coverage is especially valuable for older homes, where outdated materials or missing safety features are more likely to be present. It would cover potentially expensive necessary upgrades to roof decking, attic ventilation, and chimney crickets.

If you’re confident your home already meets modern building codes, this coverage may be less essential, but it’s worth discussing with your agent.

Key Takeaways

-

- Location, age, and materials matter. Older homes with higher-risk features cost more to insure.

- Claims history follows you. Past claims are logged in CLUE and impact rates even if you switch carriers.

- Weather risk inflates premiums. In Kansas and other hail-prone states, weather elevates rates.

- Your roof greatly affects your premiums. Newer, impact-resistant roofs can significantly lower your premiums.

- Not all carriers offer the same discounts. Ask your agent about new roof discounts, impact-resistant shingle savings, and other options.

- Inflation affects everyone. Rising material costs increase premiums irrespective of claims.

- Always ask your agent directly. Your home and risk profile are unique: there’s no one-size-fits-all for home insurance.

By asking the right questions, home insurance premiums can become less daunting and more approachable. If you’re considering filing an insurance claim on your roof, contact a trusted roofer who will assess your roof and who can provide you with the information you need to make an educated decision.

This article is part of our ‘How To’ Series. Learn more about:

Installation of Roof Components

Building Science & Roofing Systems

Home Insurance